Login

Login

Cart

Cart

Technology has been advancing and collaborating to create a genuine warrior framework that may greatly increase your capabilities. Mobile applications and eCommerce have been working together to make your life easier and more comfortable.

In the end, eCommerce moved on to collaborate with Fintech and digital payments, enabling you to conduct transactions at any moment and at any place. Nowadays, Blockchain technology is used to track transactions.

In fact, predictions indicate that the industry for blockchain technology will develop rapidly in the years to come, reaching a value of over 39 billion dollars by 2025.

According to Statista, one of the first industries to invest in blockchain was the banking industry, which now accounts for around 30% of the market value of the technology.

Blockchain’s ability to solve eCommerce problems is undeniable, from the removal of middlemen to simplified operations and decreased complexity.

But getting too deep into a subject like a blockchain technology and blockchain in eCommerce platforms may quickly become perplexing. We have summarized the key points of what blockchain is and the ways of implementing blockchain applications in eCommerce.

What Is Blockchain?

Although blockchain has been a popular term for some time, there is still a lot of misunderstanding over what it really is. Blockchain is neither a kind of cryptocurrency nor a programming language, despite being closely related to Bitcoin.

So what precisely is it?

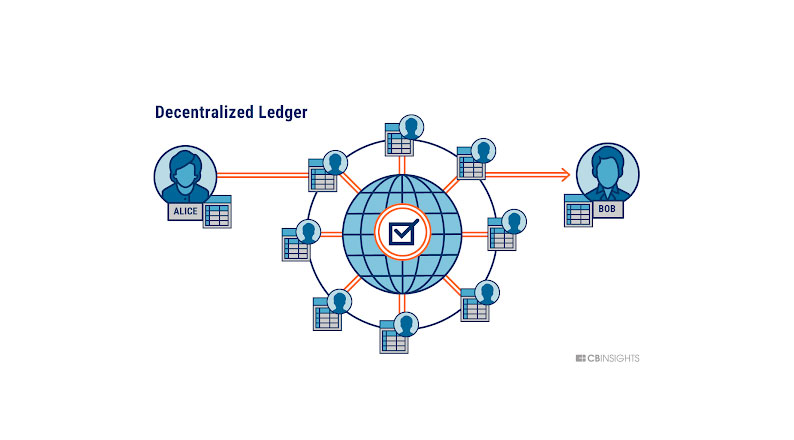

A blockchain is a shared distributed database or ledger between computer network nodes. A blockchain serves as an electronic database for storing data in digital form, including digital assets like cryptocurrencies and digitized physical assets.

The most well-known use of blockchain technology is for preserving a secure and decentralized transaction record in cryptocurrency systems like Bitcoin.

The novelty of a blockchain is that it fosters confidence without the necessity for a reliable third party by ensuring the integrity and security of a log of data.

While blockchain has historically been most closely linked with Bitcoin transactions, numerous businesses are now starting to realize its actual potential. According to Gartner, the value that blockchain will provide to businesses will increase quickly, hitting $176 billion by 2025 and $3.1 trillion by 2030.

All of this is made possible by the following crucial aspects of blockchain:

- Blockchain improves data use management by extending the potential to convert insights into irreversible assets.

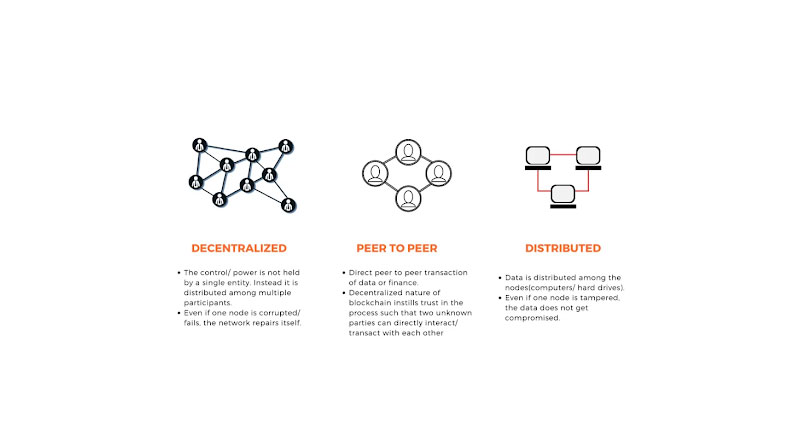

- The decentralized ecosystem gives a solid framework that is 100 % secure and almost incorruptible.

- In the absence of a central authority, blockchain establishes consensus-based trust and increases transparency.

- It makes it possible for customers to communicate directly with businesses or other customers, cutting out intermediaries.

Commonly Used Blockchain Technology in eCommerce

Ethereum and Bitcoin are the two blockchain technologies most often employed in the eCommerce industry when it comes to ways blockchain can be applied to eCommerce, and nowadays it has become inevitable that your web design company is fully aware of block chain technology too.

Customers may make purchases on websites and applications that accept Bitcoin as payment, while Ethereum offers a platform for eCommerce firms who wish to manage their own blockchains. Bitcoin was the cryptocurrency that inspired the creation of blockchain technology.

Here is further information on how Blockchain technology is often utilized in eCommerce.

1. Ethereum

Ethereum is a decentralized platform that supports smart contracts, which are programs that execute as intended with no chance of fraud or outside influence.

In late 2013, Ethereum was first proposed, and it was only in 2014 that it really came into existence.

Right now, from transaction records to a payment system, the global cryptocurrency market size, which is expected to grow to $3.13 billion in 2026 at a CAGR of 14.2%, needs the Blockchain to evolve with the growing trend, particularly in the Ethereum market.

Ether, a cryptocurrency whose value is set by the market, powers Ethereum.

Because it doesn’t need any previous expertise or understanding of blockchain technology, Ethereum is unique in that it lets developers write smart contracts.

Through a robust decentralized system, Ethereum enables the audience to communicate directly with one another. Together, the network of tens of thousands of units creates a single, robust, decentralized supercomputer.

2. Bitcoin

Bitcoin was developed by Satoshi Nakamoto, a person or group operating under a pseudonym who first described the concept in a white paper in 2008. The idea behind bitcoin, which enables safe peer-to-peer transactions online, is deceptively straightforward.

Blockchain is a public distributed ledger where transactions are recorded and cryptographically validated by network nodes. Because there are only 21 million of them, bitcoin is definitely unique.

Bitcoins are produced as a reward for the mining process. They may be traded for goods, services, and perhaps other currencies.

Over 100,000 shops and sellers accepted bitcoin as payment as of February 2015, including Microsoft, Expedia, and Twitch.

Bitcoin is basically a peer-to-peer service, so payments may be transmitted securely to their intended recipient. With their participation in internet commerce now possible, marketers from emerging nations should see a boost in business.

3. Ripple

Established in 2012, Ripple is a digital, decentralized platform system for payments.

It was released on the market to support international payments by using blockchain technology. The Ripple App’s primary goal is to facilitate safe transactions between banks and users.

The current banking system was created in the digital age of technology and has gained broad recognition for the effectiveness of its services. To move money from one nation to another at any time or location, it may take into account a variety of trusts.

Since Ripple was founded with the goal of securing bank transactions more quickly and comfortably, it is a more successful cryptocurrency choice for large financial institutions.

Although Ripple is often used to refer to the XRP coin, the majority of the XRP is actually operated by a corporation. Business and financial organizations may work together on a variety of tasks that facilitate transfer payments thanks to the Blockchain Development system connected with Ripples.

In order to save expenses while utilizing cryptocurrency transactions, the Ripples Blockchain system combines a transaction system of banks with financial organizations.

7 Ways Blockchain Can Be Applied to eCommerce

When blockchain technology and eCommerce are used together, you’ll see that it can handle product searches, selection, transaction processing, and other tasks digitally, providing consumers with a pleasurable and secure experience.

Blockchain technology has clear benefits for eCommerce. Below, we’ll discuss the application of blockchain to eCommerce and how this can benefit you.

To Improve Security for Customers’ Data

Blockchain technology can be applied to eCommerce in order to improve the security of customers’ data.

Blockchain’s Distributed Ledger Technology (DLT) provides great security for online database systems, which makes it suitable for use in eCommerce.

Additionally, there haven’t been many data breaches reported in systems powered by blockchain.

Blockchain-based currencies don’t display personal details, which is another important benefit it provides for eCommerce enterprises.

In reality, a transaction from the client’s wallet to the receiver’s wallet is authorized by the client. The sole identifying information is a randomly generated unique identification that is linked to each user’s wallet.

Today, data loss from clients is unavoidable, given the tenfold growth in cyberattacks and data breaches.

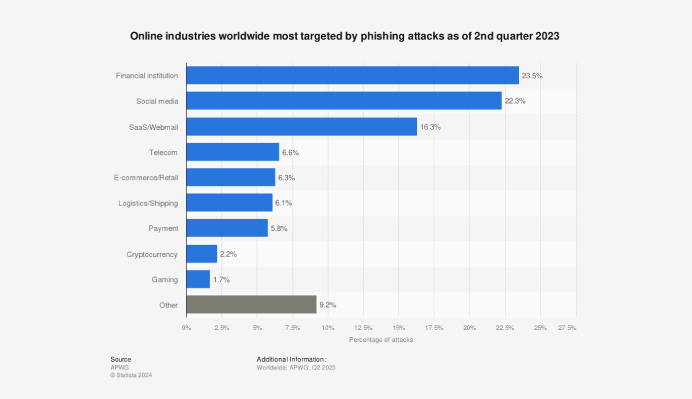

In fact, according to Statista, 6.3 per cent of phishing attacks globally during the second quarter of 2023 targeted the retail and eCommerce sectors.

And although phishing is often one of the primary methods used by hackers to take over eCommerce sites, many proprietors of such businesses are unaware of how big of a danger it is to their operations.

Therefore, using blockchain is crucial to overcome these attacks and enhance security and customer experiences.

2. Blockchain Can Reduce Shipping Costs

The ability of blockchain technology to lower shipping costs is one of its main advantages.

Real-time tracking, cargo data visibility, quicker receipts with fewer mistakes, and lower costs are the major features of shipping processes.

Blockchain technology may be used in these shipping processes to monitor shipments and packages, which might help the eCommerce industry save money on shipping. Online retailers could undoubtedly save a ton of money with this.

Distributed ledger technology allows transportation businesses to trace goods from point A to point B more precisely and effectively, which lowers costs for producers and consumers.

Since shipping costs are one of the major barriers to online shopping, this might have a huge effect on the eCommerce sector.

In fact, a 2021 European survey revealed that seven out of ten online buyers would abandon a purchase due to exorbitant delivery prices.

According to a 2024 statistical report on cart abandonment by the Baymard Institute on US Adults, the primary cause of cart abandonment is the extra costs like shipping, tax, and transaction fees being too high.

Cart Abandonment Rate Statistics – Image Source: Baymard Institute

However, adopting blockchain to control the supply chain automatically reduces costs incurred in the process. Additionally, blockchain might be utilized to develop brand-new eCommerce systems that are independent of conventional delivery techniques.

Lowering shipping costs for the majority of eCommerce companies would also assist the logistics industry.

3. Ensuring Transparency in the Supply Chain

Several brands have recently been the target of criticism after accusations of a lack of transparency.

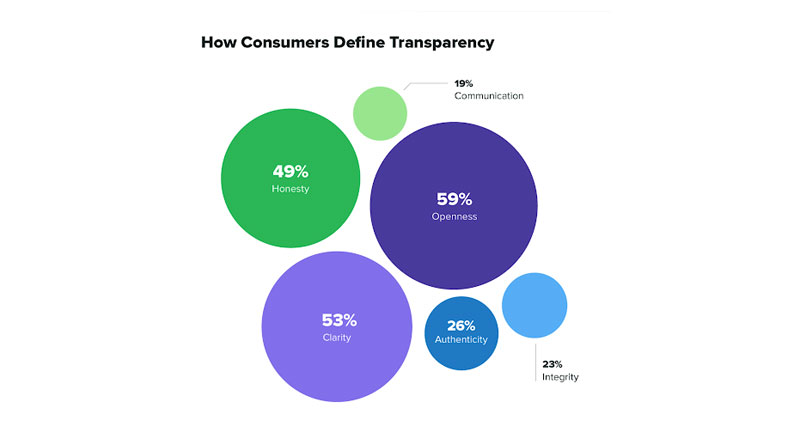

This is evident by the fact that only one in six (15 percent) consumers believe brands are currently “very transparent” on social media.

Given that the majority of consumers feel that transparency occurs when brands are open (59%), clear (53%), and honest (49%), this poses a big problem for the present eCommerce systems.

As a result, using blockchain technology in the eCommerce sector would create a decentralized setting where any guilty party on the side of the company or merchant could be effectively monitored.

It is applicable to each link in the supply chain, including the producer, distributor, retailer, and final customer.

With the help of this technology, your customers will be able to discover the explanations to all the pertinent questions, including where the items come from, who manufactured them, and exactly how they were manufactured.

As a business owner, you can enhance your brand’s reputation by taking the initiative. Using blockchain in eCommerce enables you to make your supply chain transparent management transparent and improve customer trust.

Everyone who has been given authorization has the ability to review and observe each stage of the transaction. This approach increases audience confidence and makes the transactions being conducted visible.

4. Speeding Up Transactions and Checkouts

Traditional transfers sometimes take a lengthy time, particularly when moving money between countries, which might take several days.

Contrarily, Bitcoin transactions just take a couple of minutes. Most significantly, a transaction might be completed at nearly any moment, in an instant, since they are never closed.

Thus, Blockchain technology may be used to handle and store client payment information, accelerating and securing the checkout process.

Online retailers are responding overwhelmingly to eCommerce platforms. Millions of items are added every year to satisfy consumer demand. Almost all nations will see a rise in the size of the global online retail sector.

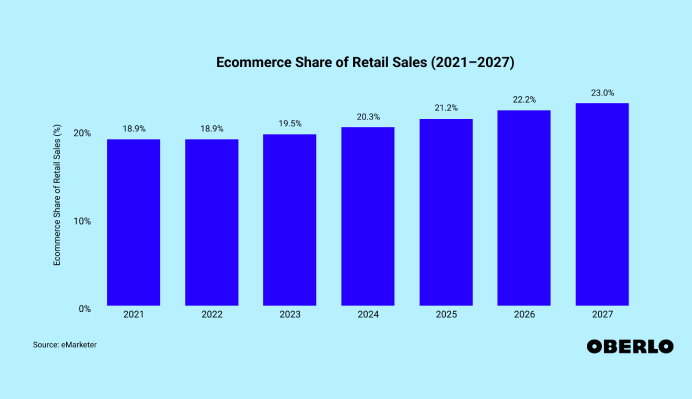

In 2023 alone, eCommerce made up about 19.5% of all retail sales globally.

According to projections, the online market will account for 20.3% in 2024 and is expected to hit 23% by 2027.

The popularity of online shopping and the rising desire for quicker checkout procedures are the main drivers of this increase.

The capacity of blockchain to provide a tamper-proof log of transactions is one way it may accelerate checkout operations in eCommerce.

Businesses may well be able to avoid having to ask consumers for personal information like their credit card details when they check out, saving them time and effort.

5. Blockchain Eliminates the Need for Middlemen

Why are we required to pay a third party a hefty additional charge to conduct a financial transaction between two or more parties that have already made an agreement when we can rely on blockchain to carry out those procedures more effectively and securely?

Before blockchain, trading needed a middleman, such as a bank or a broker that kept your financial information on their systems. A banker links to the account of the company when you transfer money or make a transaction to register the transaction.

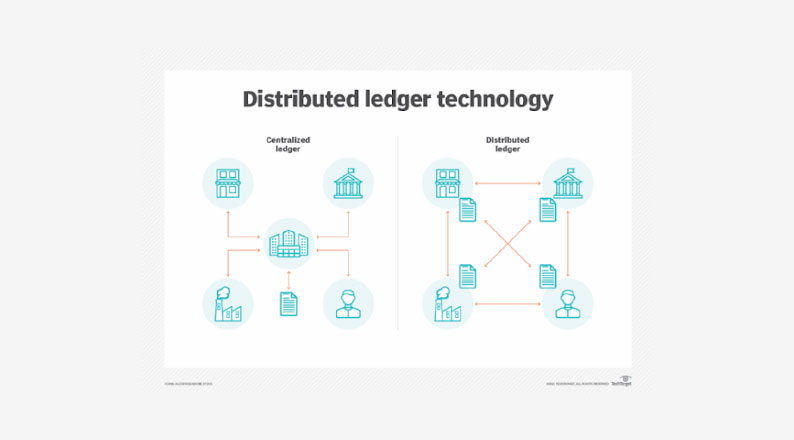

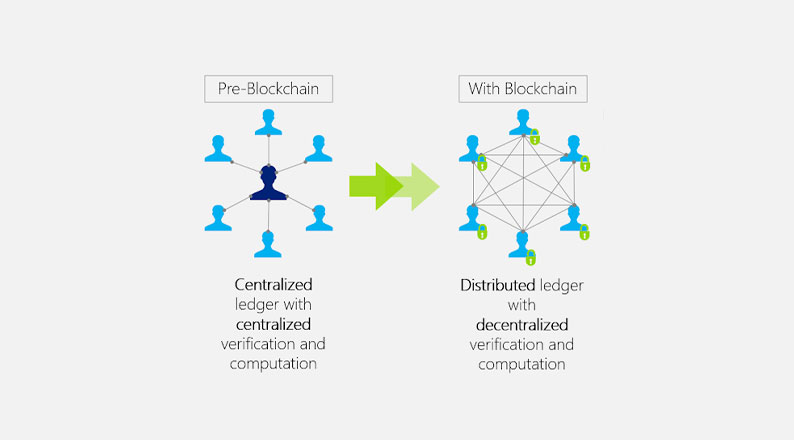

Blockchain, on the other hand, substitutes a decentralized ledger of linked records for this controlled method.

There is a verifiable history of every transaction since each record is linked to the previous one and the one following it. No record can be removed, and no record that already exists cannot be changed.

For example, in blockchain technology, the seller’s computer checks the blockchain record maintained on hundreds of other computers to determine whether the buyer holds the appropriate amount when a bitcoin transaction is performed.

A new data entry is added to the network, indicating the transfer if there is distributed consensus across the machines.

Additionally, businesses are rushing to create Direct to Consumer (DTC) channels since revenue growth is still difficult, with nearly all of them (87%) believing that these channels are appropriate for their products and consumers.

6. Blockchain Can Be Used To Ensure Product Delivery

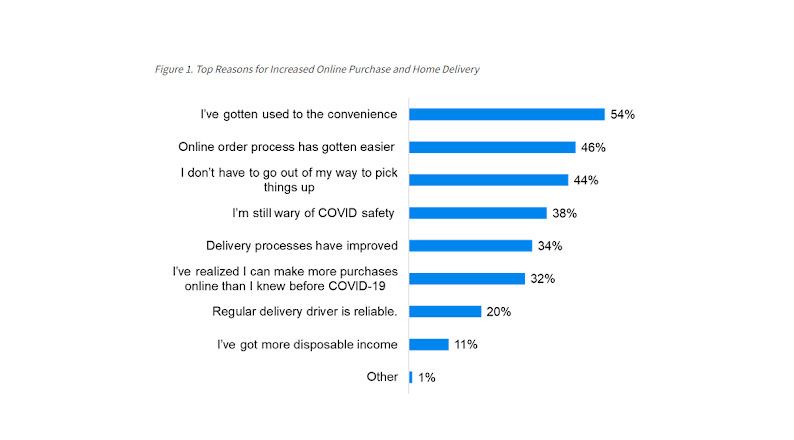

Even though there has been a rise in online purchases and deliveries, just 34% of customers indicated that delivery procedures have become better.

However, with blockchain technology, these figures are likely to change since one of the numerous benefits is the assurance of product delivery.

As everyone is aware, the discrepancy between promise and delivery has a significant effect on both satisfaction and long-term engagement with the business.

A bad delivery experience would prohibit 85% of online buyers from making another purchase from that online merchant, which shows how important delivery quality is to future purchases.

By tracking product position throughout the delivery process using IoT tagging and managing to deliver the products in real time, blockchain enhances the delivery experience for your customers.

A decentralized, encrypted database of user interactions and preferences that is real-time accessible enables it to offer seamless omnichannel engagements.

Blockchain in eCommerce guarantees that items are delivered in the anticipated timeframe since less time is required for data validation, freeing up more time for the supply of goods and services.

7. Providing Easy Access to Receipts and Warranties

Consumers often struggle with warranties.

However, it’s important to keep in mind that the warranty has two unique functions: first, it reduces the manufacturer’s potential responsibility that would arise if there was no written guarantee linked to the goods, and second, it clarifies to the customer what coverage is left over and how to get it.

Consumers often disregard warranties for certain items; therefore, the guarantee primarily serves the manufacturer’s interests.

Blockchain technology enables shops to transfer product warranties from paper-based documents to the cloud.

Warranteer is an example of a service that transfers product warranties from paper to the cloud through blockchain, keeping them valid and transferrable, and it is already being utilized by an increasing number of consumer-focused businesses.

Customers may manage a digital warranty wallet, which relieves merchants and manufacturers of administrative duties.

Blockchain technology for eCommerce also keeps track of each customer’s receipt and extended warranties.

Your audience will find it handy to save and access all of the warranty validations for their goods online as a result. With blockchain, these receipts and warranties may be easily handled.

Bottom Line

If you own an online store and want to increase efficiency, you should use blockchain technology. It will not only change how you operate but also address all your problems and come up with a permanent solution that you can follow.

The potential of blockchain is enormous, and as more and more sectors adopt the technology, its influence will only increase rapidly.

The emergence of blockchain has already begun to alter the e-commerce sector, and in the next years, it will radically change the environment of online buying. By removing intermediaries and streamlining the process, the technology will enable consumers to interact directly with shops.

There are many other ways blockchain can be applied to eCommerce, as discussed in this article, as well as the reasons why you should adopt them for your eCommerce business.

Through this article, we hope we have successfully enlightened you about the idea of blockchain technology in eCommerce.

Acowebs are developers of Woocommerce bulk discounts that will help you add bulk discounts to products on your stores. It also has developed various other plugins like the popular plugin for managing the checkout form fields in WooCommerce, called Woocommerce Checkout Manager, which is highly feature-oriented yet lightweight and fast. There is also a free version of this plugin available in the WordPress directory named W0ooCommerce Checkout Field Editor.